5 habits that teach kids the value of money

Five concrete habits that teach children about saving, budgeting and financial responsibility — without turning it into dull pedagogy.

Most parents agree that children should learn about money. Fewer have a clear plan for how. And very few succeed — not because they’re doing something wrong, but because money for children is more about habits than about conversations. You can explain to a child what interest is for 45 minutes and still not make it stick. But if your child has saved their own money for a bike over twelve months, she has learned more about saving than a whole school lesson could ever give.

Here are five habits I’d single out — based on what I see working among families using the Ukelønn app, and not least among families we know personally. They’re simple. They don’t require a personal financial adviser. But they work, over time.

1. Make the budget visible

Children don’t understand money they can’t see. That’s fundamental. If dad pays for everything by card, and money just sort of “appears” whenever something needs buying, money becomes something abstract. The child never learns that the family is actually making choices.

The simplest version: show your child where the money goes. Not the details, but the big picture. “This is how much food costs each month. This is what rent is. What’s left over, we divide between holidays, activities, clothes and unexpected things.”

For children aged 9–10 you can get even more concrete. Show them how much electricity cost over the winter. Show them what the annual football club membership is. Let them see that everything is a choice.

Some parents are afraid of “worrying their child with money”. But hiding it has the opposite effect. Children who have never seen a budget grow into young adults who don’t understand why mum and dad sometimes say no. They learn that money is something mysterious — not something you manage.

2. Set savings goals the child can watch grow

Saving is hard because it’s abstract. A child saving 1,500 kr for a bike doesn’t need to hear “it’s good that you’re saving”. The child needs to see how close the goal is.

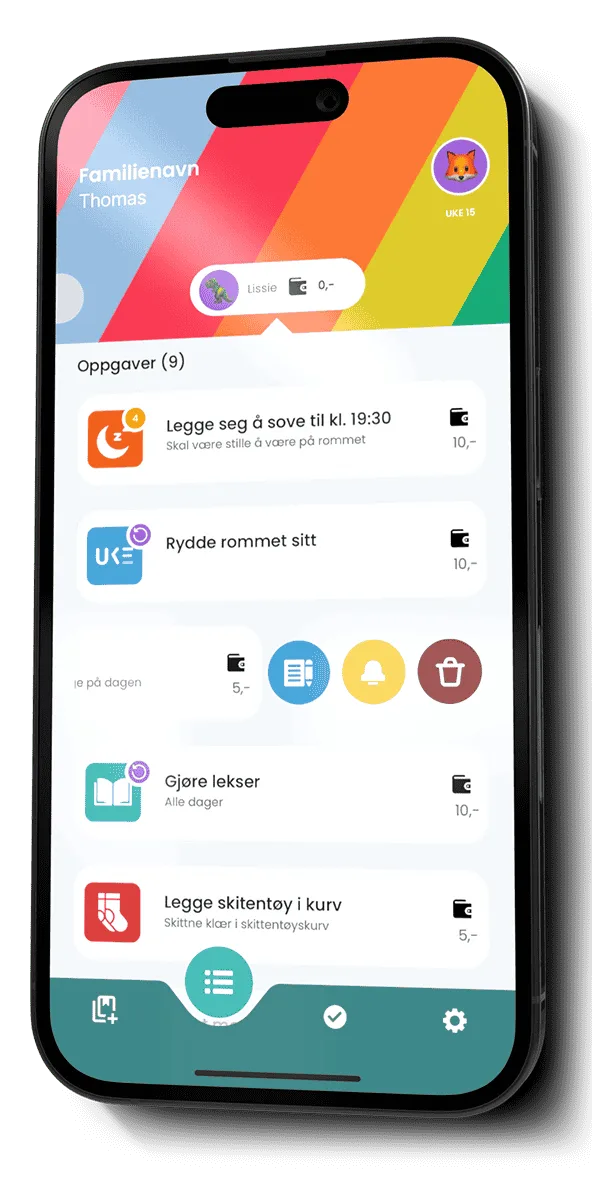

This works because the human brain is wired for the visual. A thermometer drawing on the fridge — where the child colours it in every time she adds money — is more motivating than a number in an app. But a digital progress bar, like the one we have in Ukelønn, does the trick too. The point is that the child should have something to check, something to be inspired by.

One concrete tip: don’t pick a savings goal that’s too far away. For a 7-year-old, three months is an eternity. Choose something achievable in 4–8 weeks. Once they’ve experienced just once that “I saved, and I got it” — the motivation for bigger goals follows almost by itself.

3. Teach the 10/10/80 rule

This is an old rule of thumb: for every hundred kroner the child receives, 10 kr goes to gifts or charity, 10 kr to savings, and 80 kr to free spending.

I know what you’re thinking. That’s too simplistic. And yes, it is. But it’s also a starting point that actually works for children, because it’s mechanical and easy to remember. An 8-year-old can manage 10/10/80. She can’t manage a nuanced discussion about short-term versus long-term consumption.

I’d adjust it slightly:

- 10% to gifts and charity: This isn’t just about giving away, but about choosing who you want to help. Let the child choose. Maybe a best friend’s birthday, maybe a children’s charity like Save the Children, maybe a distant aunt. The choice is the point.

- 10% to long-term savings: This is saving that isn’t meant for small things. It could go into BSU (a Norwegian tax-favoured savings account for young people — more on that in tax, saving and allowance), or a separate account that only opens at 18.

- 80% to spending: This is the money the child controls themselves. Including savings goals for a bike, games or other shorter-term things.

As the child gets older the split can shift — maybe 20/20/60 or 30/30/40. But the principle that everything coming in gets allocated is the most important part.

4. Celebrate milestones, not amounts

One of the most surprising things I’ve learned from building Ukelønn is that children aren’t motivated by numbers. They’re motivated by meaning.

Let me illustrate. Two statements:

- “You’ve saved 500 kr.”

- “You’ve saved half of the bike — if you keep going you’ll reach your goal by the summer holidays.”

The first is a fact. The second is a story. Children — and honestly adults too — are motivated by stories, not facts.

When your child reaches a milestone: make a bit of a fuss about it. Don’t buy anything — just tell it as a story. “Remember four weeks ago when you decided on this bike? Now you’re halfway there. You’ve actually saved more than dad did when he was 9.” That kind of comment sticks. It teaches the child that what she does matters.

5. Let them make mistakes — with small amounts

This is the hardest habit, because it requires you to keep quiet.

Children don’t learn about money by being warned. They learn by making mistakes. If your 11-year-old has saved for three months and decides to buy a game you know he’ll regret — let him buy it. Let him feel the regret. Let him explain to you three weeks later why it was a bad idea.

The problem with always protecting your child from bad purchases is that you become the one carrying the financial sense. The child never learns to judge for himself. When he’s 22 and living alone, that’s the first time he actually has to face the consequences of his own choices. That’s late.

Two rules for this:

- Small amounts. Don’t let the 8-year-old blow the entire savings pot on sweets he’ll regret. But 50 kr on something silly? Let it go. That’s the lesson.

- Talk afterwards, not before. Warning before the purchase feels like nagging. Reflecting together afterwards feels like a conversation. “Was it worth it? What would you do differently?” Not as criticism, but as curiosity.

I’ve seen children learn more from an 80-kroner bad buy than from hours of parental lecturing.

It’s not the app that teaches kids about money

I’m going to sound contradictory saying this, but I mean it deeply: no app can teach children about money. Ukelønn is a tool that supports all five habits above. It makes it easier to set savings goals, easier to make money visible, easier to split things into spending and saving. But the principles matter more than the app.

If you don’t use Ukelønn and never will — no problem. All five habits can be done with a marker pen, a sheet of paper and a box in the cupboard. What counts is that you do them, consistently, throughout childhood. Then your child learns about money in a way no school lesson can match.

What should you do this week?

If you want to start somewhere, I’d begin with points 1 and 2. Make the budget a little more visible — just a simple extract on the fridge, nothing dramatic. And set one savings goal together with your child, with visual progress.

The other three habits can follow. Rome wasn’t built in a day, and neither is a childhood.

If you’d like to read more, take a look at how much allowance in 2026 or tax, saving and allowance for the more practical side of things.